Do you want to get the monthly income out of your investments without tying up all your money in the form of fixed deposits or without selling all the assets simultaneously? One of the most intelligent methods of earning a regular income, while still having your money invested, is a Systematic Withdrawal Plan (SWP).

In this detailed guide, you’ll learn what SWP is, how it works, and how to select the most suitable SWP plan when investing each month. I will also demonstrate to you how to calculate correctly what you will earn each month using an SWP calculator to be able to plan your budget.

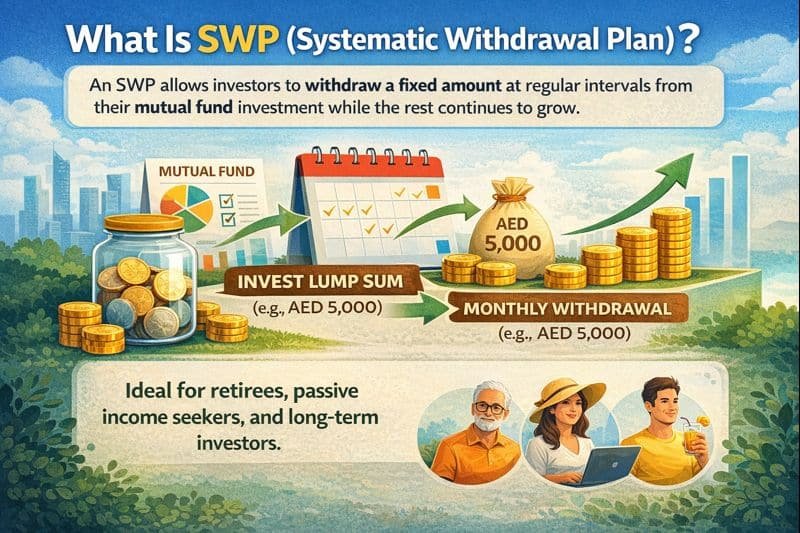

What Is SWP?

An SWP (Systematic Withdrawal Plan) is a system provided by mutual funds that enables an investor to take a certain amount of money out of the investment in a regular period, often monthly.

SWP also allows you to receive a small amount of money at a time, but leave the rest of the money invested and keep earning.

Simple SWP Example

- You deposit a sum of money in a mutual fund.

- You choose a specific sum of money per month to withdraw (e.g., AED 5,000).

- Redemption of units corresponding to the same is done every month.

- The rest of your investment continues to grow

This renders SWP as a perfect choice among retirees, passive income earners, and long-term investors.

How Does an SWP Work?

An SWP works in a structured and automated way:

- You deposit a sum of money in a mutual fund.

- You choose the withdrawal amount and frequency (monthly, quarterly, etc.)

- The fund sells off fewer than a few units periodically.

- Income comes into your bank account regularly.

- The rest of the investment remains invested.

Since these are systematic withdrawals, SWP enables you to eliminate the risks of market timing as well as have a fixed stream of income.

Benefits of SWP for Monthly Investment

Systematic Withdrawal Plan has several benefits:

- Dividend revenue every month without having to sell all the investment.

- Most efficient withdrawals in terms of taxation over traditional income alternatives.

- Anytime flexibility of changing or halting withdrawals.

- Long-term potential is better than that of fixed deposits.

- Perfect when it comes to retiring and being financially independent.

All these advantages make SWP one of the most appropriate strategies for investors who desire income without sacrificing growth.

Read Also: Avoid Losing Your UAE Gratuity: 9 Flaws That Trigger Denial

Best SWP Plan for Monthly Investment

The optimal SWP plan is based on your risk level, income requirement, and investment time horizon.

Key Factors to Consider

- Monthly income requirement

- Investment duration

- Risk appetite (low, moderate, high)

- Market conditions

Best Types of Mutual Funds for SWP

- Debt Funds: These are appropriate for investors who are conservative and require stable income.

- Hybrid Funds: Balance between growth and stability

- Equity-Oriented Funds: These are the funds that are appropriate for long-term holders of investments who seek to get income in a way that beats inflation.

The key to any successful SWP is to select the appropriate type of fund to make sure that it will serve longer and provide a constant source of income.

How Much Monthly Income Can You Get from SWP?

The monthly SWP income is determined by:

- Total investment amount

- Expected rate of return

- Withdrawal amount

- Duration of withdrawals

To have a clear and accurate estimate, one can use this free SWP Calculator, which was created in the case of UAE investors:

This tool helps you calculate:

- Monthly withdrawal amount

- Remaining investment value

- Investment longevity

Financial planning is easy, quick, and accurate with the help of an SWP calculator.

SWP Example: Monthly Income Illustration

Let’s understand SWP with a realistic example:

- Investment Amount: AED 500,000

- Monthly Withdrawal: AED 5,000

- Expected Annual Return: 8%

Through an SWP, you get the regular monthly income with the balance of your investment growing so that your money will go further than your normal withdrawal mode.

SWP vs SIP vs Dividend Plan

| Feature | SWP | SIP | Dividend Plan |

|---|---|---|---|

| Purpose | Monthly income | Wealth creation | Periodic payouts |

| Control | High | Medium | Low |

| Tax Efficiency | High | Moderate | Low |

| Ideal For | Retirees | Long-term investors | Income seekers |

This comparison shows why SWP is often preferred for a predictable monthly income.

Who Should Invest in an SWP?

SWP is suitable for:

- Retired individuals

- Investors seeking passive monthly income

- People planning long-term withdrawals

- Those investors are interested in tax-efficient income.

SWP can be a very good option in case you need income but not growth.

Frequently Asked Questions (FAQs)

Is SWP safe?

The safety of SWP is related to the kind of mutual fund one selects. Debt and hybrid funds tend to be less risky when compared to equity funds.

Can SWP run out of money?

Yes, when the withdrawals are too great or the returns too small. This is avoided through proper planning.

Is SWP better than fixed deposits?

SWP can also be more tax-efficient and a better growth prospect in terms of long-term income.

What is the minimum investment for SWP?

It depends on the fund, but most mutual funds permit SWP and have tolerable minimum investments.

Can I change my SWP amount?

Yes, SWP is flexible to make or disrupt withdrawals at any time.

Read Also: Gratuity in Salary 2026: Complete Guide to What You’re Owed

Final Thoughts

A Systematic Withdrawal Plan is among the best methods of earning a monthly income and having your investments grow at the same time. With the help of a SWP calculator, the correct selection of a fund, and determining an amount of withdrawal at a sustainable rate, you can create a stream of income that will correspond to your financial aspirations.

Smart planning today can ensure financial peace of mind tomorrow.