Have you been asking yourself what DBR on your bank statement is? You have probably come across the acronym DBR in the process of seeking a loan or reviewing your banking materials, and the meaning behind the acronym may not be obvious all the time. A critical parameter that is used to evaluate your debt handling capability by banks is the DBR, or Debt Burden Ratio. Knowing the DBR is important not only for loan approval but also in making wise financial choices and enhancing the borrowing capacity.

In this guide, I will provide all about the meaning of DBR in banking, demonstrate how this ratio is calculated, why it is important, and give practical tips to work towards a better DBR.

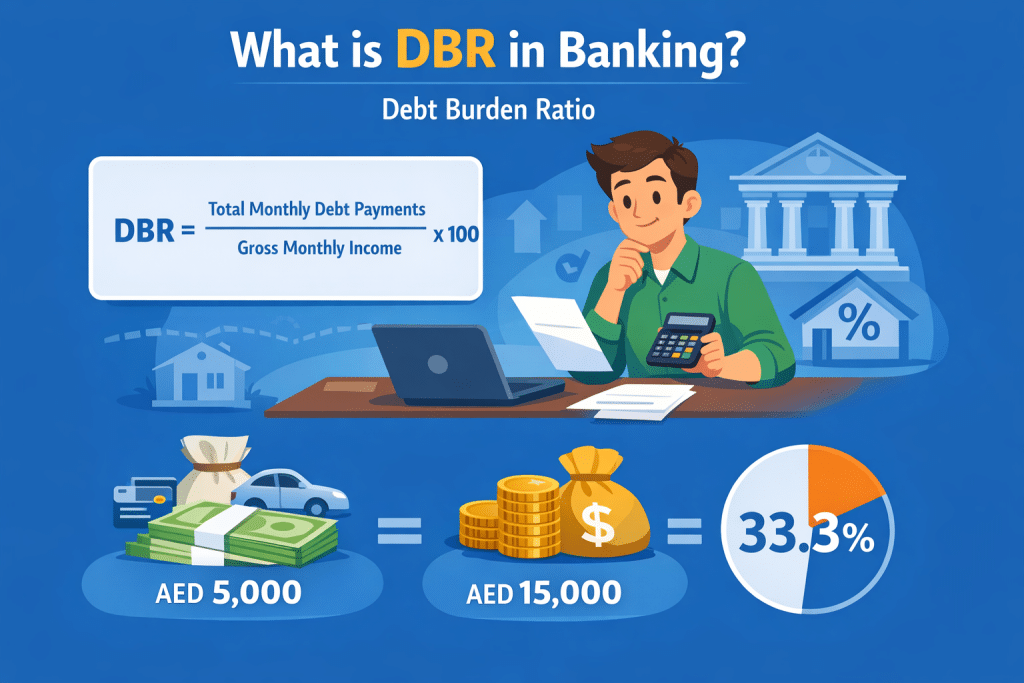

What is DBR in Banking?

Definition of DBR

DBR is an acronym that is also known as Debt-to-Income Ratio. It is a financial indicator and a bank measure of the proportion of individual income that is spent on settling debts. Basically, it is a test of your capacity to accept new loans without straining your budget.

Formula: DBR = Gross Monthly IncomeTotal Monthly Debt Payments×100

For example, if your total monthly debt payments are AED 5,000 and your gross income is AED 15,000:DBR = 150005000×100=33.3%

This implies that you would be paying on your debt 33.3 percent of your earnings.

How is DBR Calculated?

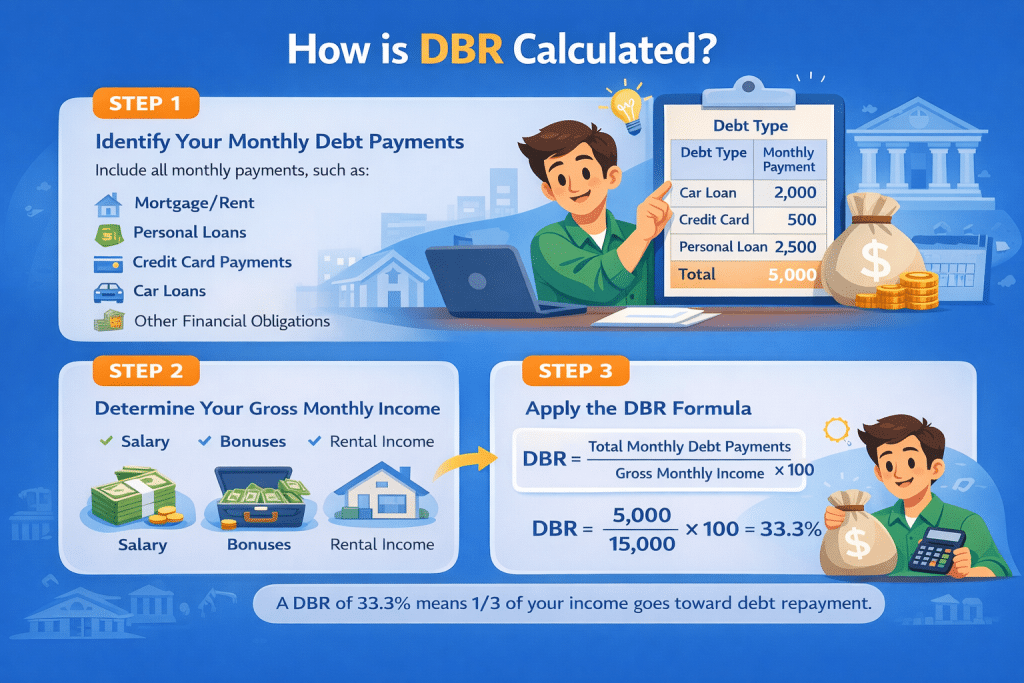

Step 1: Identify Your Monthly Debt Payments

Included in all monthly payments, including:

- Mortgage or rent

- Personal loans

- Credit card minimum payments

- Car loans

- Other financial obligations

Example:

| Debt Type | Monthly Payment (AED) |

|---|---|

| Car Loan | 2,000 |

| Credit Card | 500 |

| Personal Loan | 2,500 |

| Total | 5,000 |

Step 2: Determine Your Gross Monthly Income

This includes the sum of the income before taxes or deductions, and is:

- Salary

- Bonuses

- Rental revenue or other recurrent revenue.

Example: AED 15,000

Step 3: Apply the DBR Formula

DBR=GrossMonthlyIncomeTotalMonthlyDebtPayments×100

Using the example: DBR=15,0005,000×100=33.3%

Interpretation: A DBR of 33.3% implies that you are paying off debts with one-third of your income. The majority of banks will want a DBR to fall below 40-50 percent, depending on the regulations in the area. You can also use our DBR calculator.

DBR in UAE Banks

Typical DBR Limits in UAE Banks

- The UAE banks suggest that one should have a DBR of less than 50% in personal or home loans.

- Some banks can give a higher DBR in case you have other income or assets.

- The UAE Central Bank keeps a check on DBR to keep the financial stability level intact and safeguard the borrowers against over-indebtedness.

How Banks Use DBR for Loan Approvals

- Loan eligibility: Banks will determine DBR and then proceed to approve personal loans, auto loans, or home loans.

- Interest rates: An increase in DBR can cause an increase in interest rates or a reduced size of loans.

- Risk assessment: Low DBR represents low financial risk, which augurs well towards approval.

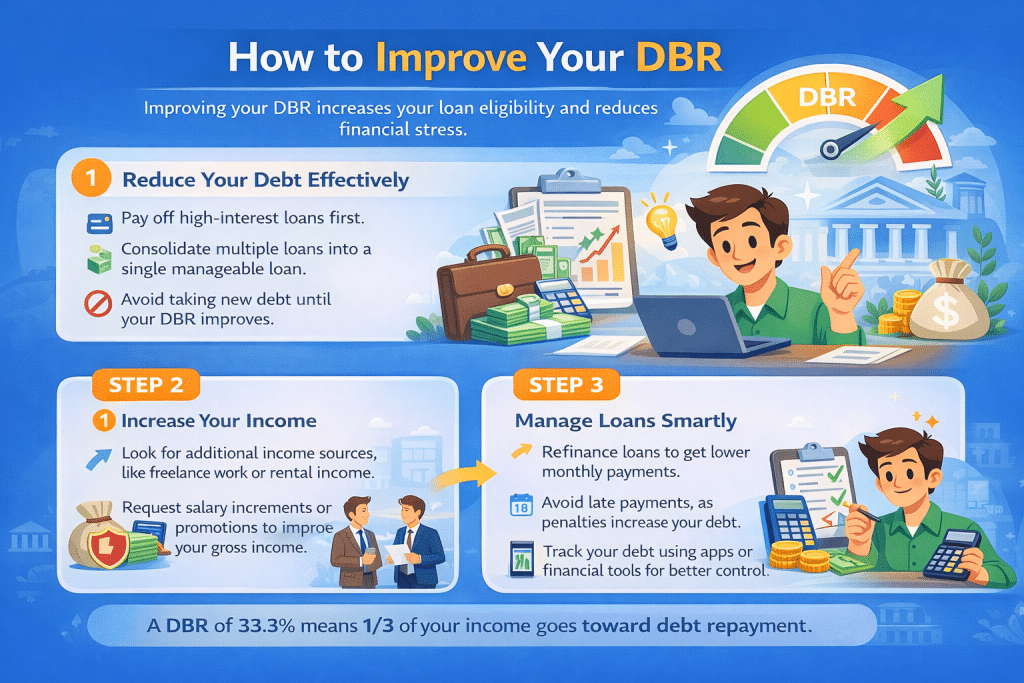

How to Improve Your DBR

The best way to improve your DBR is to make yourself eligible to get a loan and to spend less on it.

1. Reduce Your Debt Effectively

- Service high-interest loans initially.

- Bring several loans into one loan that can be handled.

2. Increase Your Income

- Find other sources of income, such as rental earnings or freelancing.

- Ask to have your salary increased or be promoted to boost your gross income.

3. Manage Loans Smartly

- Get a refinance loan to pay lower monthly payments.

- Avoid late payments, as penalties increase your debt and DBR.

- Better control of your debt would be through the use of apps or financial tools.

Common Questions About DBR

What is a Good DBR?

- The majority of banks suppose that a 30-40% DBR is safe.

- Reduced DBR will promote your loan approval.

Does DBR Affect Credit Score?

- DBR in itself has no direct impact on your credit score.

- Nevertheless, high DBR will raise the default risk, and this can affect your credit history.

Can DBR Prevent Loan Approval?

Yes. In case your DBR is excessive, banks will:

- Turn down your loan application.

- Approve a smaller loan amount

- Offer higher interest rates

Read Also: What Is SWP? Monthly Income Plan Explained

Final Words

Every borrower must be informed about DBR in banking. It assists you in themanagement of your finances, planning to apply for loans, and saving you the hassle of financial stress. Monitoring and optimizing your DBR will help not only to get more loans but also to have a better interest rate and loan terms.

It should be remembered that with a low DBR, you are not only expanding your borrowing potential, but you also have the capability of managing your finances without a lot of financial anxiety.